Ergodic & non-Ergodic Regimes

Ergodic & non-Ergodic Regimes

Time averages versus ensemble averages.

… let us recall that a dynamic system is termed ergodic if the equations describing its evolution at random initial conditions and fixed external parameters have a unique possible stationary solution. If the dynamic system is not ergodic, then its behavior over an infinitely large time interval will depend on the initial conditions. As applied to the climatic system this is equivalent to the fact that external parameters uniquely determine climate in the first case and non-uniquely in the second case.

Edward Norton Lorenz

Ergodic Theory

Distinguishing time averages from ensemble averages is a practice relevant to the behavior of financial markets and wealth, as well as the earth’s climate systems and thermodynamic physical processes. This concept has its roots in ergodic theory and in statistical physics through the work of Boltzmann, Maxwell, and Gibbs. In this post, I will describe how these insights from ergodic theory and statistical physics might inform a thermodynamic view of risk-taking and models about risk.

We recall that systems undergoing climate change are not ergodic, hence temporal averages are generically not appropriate for the instantaneous characterization of the climate. In particular, teleconnections, i.e. correlated phenomena of remote geographical locations are properly characterized only by correlation coefficients evaluated with respect to the natural measure of a given time instant, and may also change in time.

The Theory of Parallel Climate Realizations

Time Average vs. Ensemble Average

What is meant by distinguishing between the time average of a data generating process and the ensemble average of that same process? The property that the average behavior of a process at a fixed interval in time is the same as if we track one realization of it over a long period of time is called the ergodic property. The fixed interval here refers to an ensemble (many copies) of one subset of time versus a longer time series of infinite theoretical length and how its statistical parameters behave as it approaches a limit.

Another way to think of an ergodic process is that over time it visits every possible state in proportion to the probability of that state, and does so with the same proportions no matter where you start the process off.

This begs the question. Unlike the climate or other non-ergodic physical processes — are financial markets ergodic, is the time series of wealth accumulation by individuals, institutions, and societies coming from an ergodic process?

The answer seems to be no. In dealing with decision-making around stochastic, non-ergodic phenomena such as financial markets or similar, we cannot go back in time. We cannot repeat our experiments in many parallel universes as the use of statistical ensembles implies. Additionally, long tail events and other large swings in financial markets may cause extended periods of disequilibrium that are difficult to recover from. The behavior of wealth and markets share this property of non-ergodicity with certain physical processes like the climate.

A quote from The ergodicity problem in economics:

To make economic decisions, I often want to know how fast my personal fortune grows under different scenarios. This requires determining what happens over time in some model of wealth. But by wrongly assuming ergodicity, wealth is often replaced with its expectation value before growth is computed. Because wealth is not ergodic, nonsensical predictions arise. After all, the expectation value effectively averages over an ensemble of copies of myself that cannot be accessed.

Ole Peters, Nature Physics

Markov Chains, Path Dependency, and Ergodicity

How a system behaves in terms of remembering or forgetting its history will influence its ergodicity. This is known as path dependency.

Here is a simple way to illustrate a path dependent, non-ergodic system with a Markov chain. A data generating process will be non-ergodic if the outcome is dependent on where the system starts out, as is the case with this partially recurrent Markov chain.

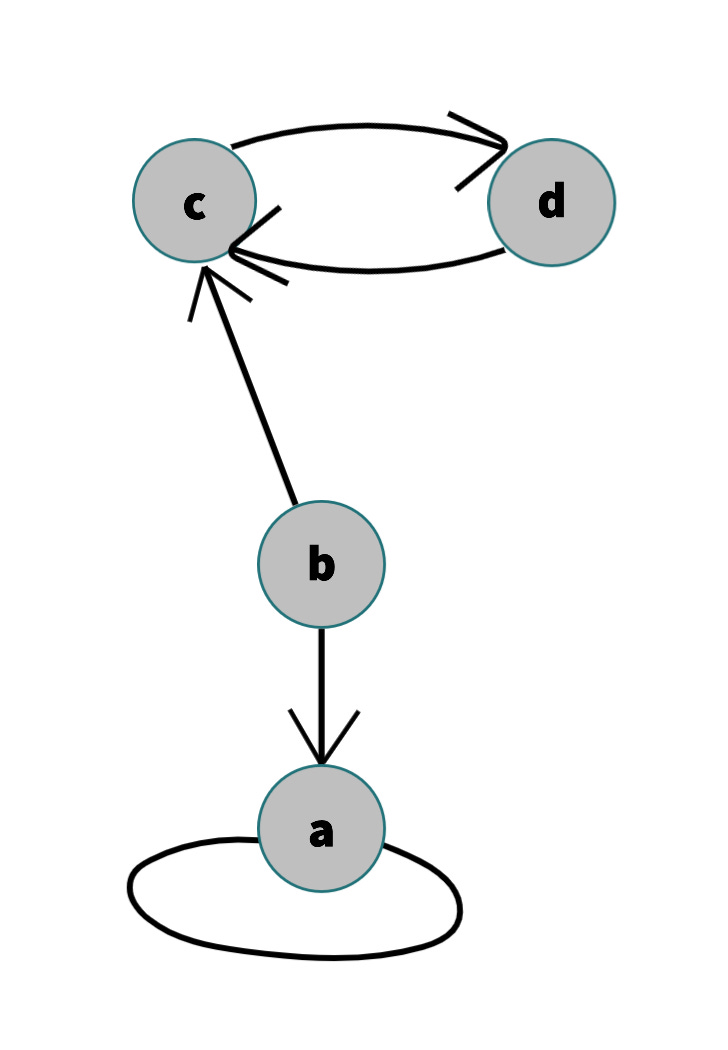

Consider this Markov chain with two recurrent classes and one transitional class:

A Markov chain with two recurrent classes, between {a} and itself and {c, d}, and a single transitional state {b}. If starting on the transitional state {b} it is a temporary state before the system relaxes into one of the recurrent classes. State changes from {b} are not bi-directional, and {a} and {c, d} are both infinite loops.

Regardless of the actual numerical probabilities for transitions, this Markov chain is not ergodic because the probability of ending up on a given state depends on the initial state and there are states that will never be explored in a single run, since they are exclusive. In the time-average running domain of this process, once you are stuck in one recurrent class you cannot realize the other. If you start out on either recurrent class {a} or {c, d} then you also just stay there. Hence there is very basic path dependency in this Markov process, which makes it non-ergodic as well. It moves in a one-way fashion that settles into two possible states and it cannot be reversed.

One would have to simulate this process many times with different initial conditions to fully understand it. The key point being that if different initial conditions are required, it is not ergodic. It has multiple regions in the state space to get stuck in. In an ergodic process, one single very long simulation should be sufficient for the process to visit all possible states, in proportion to their respective probabilities, regardless of where the simulation is started off.

In Physics & In Nature

Ergodicity is a regime; a period or characteristic behavior within a time window, in which the data exhibits a certain property. It is characteristic of certain physical processes that they are non-ergodic and then settle into an ergodic phase (diffusion-like behavior). This is a complex topic which is discussed in greater depth in the references and Physics literature listed at the end of this post, I cannot claim credit for all the nuances of this research.

(I) Ergodicity

The right side of the equation is the ensemble average over N trials, and the left side is the time average given as T approaches infinity. As the number of trials approaches infinity these two values should converge if the regime is ergodic.

(II) Birkhoff’s Equation

Another way to express the right hand side is as an expectation.

Conclusion

We should be mindful of the ergodic property when doing time series analysis and especially when analyzing decision-making and expectation values for non-repeatable experiments.

Ergodicity is also relevant under the presence of LRD (long-range dependence) in a data generating process: it takes sufficient time to learn the parameters of a process that has very long term auto-covariances, especially if they are periodic or cyclical. Auto-covariance in the process may also induce sensitivity to initial conditions since initial values remain relevant and effect values far into the future.

The ‘random’ walks of asset prices frequently appear non-ergodic, as when they exhibit long auto-correlated runs or crashes following significant tail events: in between mean-reverting behavior. These are typically significant processes that move the system further from equilibrium. The time scales over which these processes repeat or the disequilibrium resolves is an open question.

Central to decision-making under uncertainty is an approach to risk-taking. In certain cases it is better to view decisions or expected values as one-shot opportunities that cannot be repeated. It seems to touch on our relationship with time, long-range dependence, and the irreversibility of path dependent outcomes which is a line of thought I will be exploring deeper.

References & Further Reading

The Ergodicity Problem in Economics

Ole Peters, Nature Physics

Time to Move Beyond Average Thinking

Nature Physics

Effective Ergodicity in Single-spin Flip Dynamics

Mehmet Süzen

Ergodic Markov Chains

Greg Gunderson

Regimes in Simple Systems

Edward Norton Lorenz

and more in the README: https://github.com/regimelab/notebooks/blob/main/README.md#ergodicity--diffusion